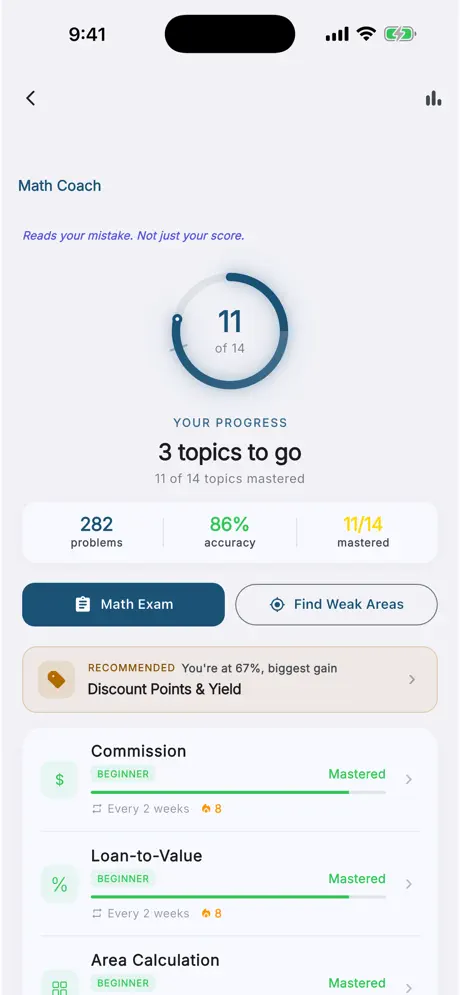

Commission & Splits

Stopping at total commission when the question asks for the associate's share.

Commission Amount

Multiply the sale price by the commission rate to find the total commission earned on the transaction.

Agent Split

Find the brokerage's side of the commission first, then apply the agent's split. Use total commission only when the question says that brokerage receives the entire commission.

Finding Sale Price from Commission

When you know the commission earned and the rate, divide to find the original sale price.

Proration

Getting the credit direction backward, or using the wrong 360 vs. 365 day count the question specifies.

Daily Rate

The Texas exam specifies whether to divide by a 360-day or 365-day year in each proration question. Use exactly what the question states.

Party's Share

Multiply the daily rate by the number of days owned in the proration period. The question tells you whether the day of closing belongs to the buyer or the seller.

Cap Rate & GRM

Using gross rent for cap rate or NOI for GRM. The exam separates gross from net.

Capitalization Rate

The cap rate measures the rate of return on an income property based on net operating income.

Property Value (Income Approach)

Divide net operating income by the cap rate to estimate value using the income approach.

Gross Rent Multiplier

GRM is a quick comparison tool for income property. Use the gross rent the question gives (monthly or annual).

Property Tax

Applying the rate per $100 before subtracting the homestead exemption from appraised value.

Taxable Value

Subtract applicable exemptions from the appraised value before applying the tax rate. Texas Comptroller guidance currently lists a $140,000 school-district residence homestead exemption, and local-option exemptions can also apply.

Annual Property Tax

Texas property tax rates are commonly stated per $100 of taxable value. If a question uses mills, a mill is $1 per $1,000.

Property Management

Using potential rent as income collected without subtracting vacancy and collection loss.

Effective Gross Income

Effective gross income is the rent a property actually collects: start with full-occupancy rent, subtract expected vacancy and uncollected rent, then add other income like laundry or parking.

Net Operating Income

NOI is the income left after normal operating expenses. Do not subtract mortgage payments, income taxes, depreciation, or capital improvements unless the question specifically directs you to do so.

Vacancy Rate

The share of units not producing rent. Multiply potential gross income by the vacancy rate to estimate the vacancy loss.

Occupancy Rate

The share of units that are rented. Occupancy rate and vacancy rate always add to 100%.

Rent per Square Foot

A per-square-foot rent lets you compare differently sized spaces. Match the period the question uses, monthly or annual.

Area & Acreage

Comparing price per acre to price per square foot before converting units.

Square Footage

Multiply length by width to calculate rectangular area.

Acres Conversion

There are 43,560 square feet in one acre (memorize this; it is not provided at the test center).

Price per Square Foot

Divide the total price by the square footage to determine price per square foot.

Interest & Loan Costs

Calculating points from the sale price instead of the loan amount, or forgetting that one point equals one percent.

Simple Interest

Annual interest equals the loan balance times the annual rate. Divide by 12 for a monthly figure.

Monthly Interest

Use the outstanding loan balance, not the original sale price. In an amortization problem, the interest portion is calculated before the principal reduction.

Loan Origination Fee

Financing fees are calculated from the loan amount unless the question gives a different base. Read the fee label before multiplying.

Discount Points

One discount point equals 1% of the loan amount. CFPB describes discount points as an upfront closing fee exchanged for a lower rate; the amount of rate reduction varies by lender, loan, and market.

Principal Reduction (Amortization)

An amortized payment contains interest and principal. Subtract that month's interest from the principal-and-interest payment to find how much reduces the loan balance.

Prepayment Penalty

Prepayment terms vary. Use this relationship only when the question supplies a percentage penalty and the balance to which it applies.

Loan-to-Value (LTV)

Using asking price instead of appraised value or sale price, whichever is lower.

LTV Ratio

LTV measures how much of the value is financed. When the exam gives both price and appraisal, use the value it tells you to (often the lower).

Down Payment

The buyer's down payment is the part of the purchase price not financed. If the appraisal is below the purchase price, the lender may base the maximum loan on the lower value, leaving an additional appraisal gap for the buyer to fund.

Seller Net & Required Price

Using equity as seller net or forgetting that commission rises as required price rises.

Seller Net

Seller net is what remains after the loan payoff, commission, and seller closing costs are subtracted.

Required Sale Price

Work backward from the seller's target. Add the payoff and fixed costs, then divide by the percentage left after commission and other percentage-based selling costs.

Buyer Cash Required

Add the buyer's down payment, closing costs, and prepaid items, then subtract any seller or lender credits stated in the problem.

Transfer Tax (National Formula)

Use the tax unit and rate supplied by the question. Texas has no statewide real estate transfer tax, but Pearson's National/General outline still includes transfer-tax calculations.

Recording Fee

Recording charges vary by jurisdiction. Use the number of pages or instruments and the fee basis given in the question.

Mortgage Qualifying Ratios

Mixing monthly and annual numbers or leaving taxes and insurance out of PITI.

Monthly PITI

PITI combines the monthly principal-and-interest payment with monthly property taxes and insurance. Convert annual taxes and insurance to monthly amounts before adding.

Front-End Ratio

Compares the housing payment (PITI) to gross monthly income.

Back-End Ratio

Includes the housing payment plus other recurring monthly debt.

Profit, Loss & Equity

Treating appreciation, equity, and profit as the same number.

Equity

Equity is the owner's value position before selling costs. It is not the same as profit.

Appreciation

Appreciation measures value increase. Debt does not change the appreciation calculation.

Market Value Depreciation

For a simple exam value-loss problem, depreciation is the decrease from the original value to the current value. Use any tax-depreciation method only when the question supplies it.

Return on Investment (ROI)

ROI compares the return identified by the question with the amount invested. Confirm whether the problem asks for annual return or total gain.

Profit or Loss

Profit includes the relevant acquisition, improvement, and selling costs supplied by the problem. It is not the same as appreciation or equity.

Adjusted Basis

For a simplified exam problem, adjusted basis starts with purchase price, adds qualifying capital improvements, and subtracts depreciation supplied by the question.

Estimated Taxable Gain

Use the sale proceeds and adjusted basis given in the problem. Real tax treatment can include exclusions, recapture, and other rules, so this simplified relationship is for exam preparation rather than tax advice.

Comparable Sales Adjustments

Adjusting the subject instead of the comparable, or reversing add and subtract.

Inferior Comparable

Add when the comparable is inferior to the subject. You adjust the comparable toward the subject.

Superior Comparable

Subtract when the comparable is superior to the subject. The subject stays fixed.

Pair this reference with the 14-area study guide and the calculator hub. For more practice, use the math drill.